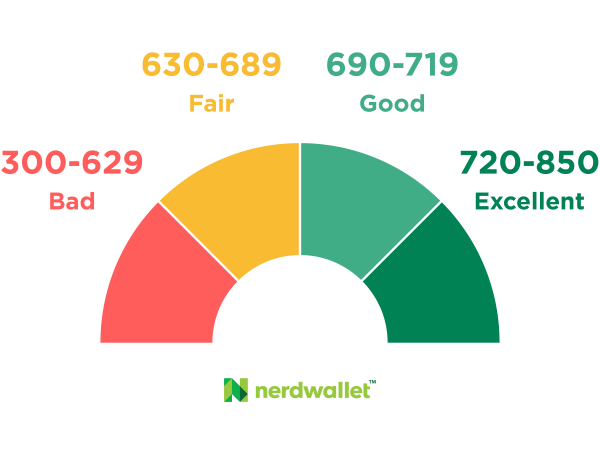

Your Credit Score Is Important

Credit scores determine whether you get loans and the rates you pay — and it pays to have a good credit score. The lifetime cost of higher interest rates from bad or mediocre credit can exceed six figures.

Someone with FICO scores in the 620 range would pay $65,000 more on a $200,000 mortgage than someone with FICOs over 760.

Since credit scores have become such an integral part of our financial lives, it pays to keep track of yours and understand how your actions affect the numbers. So do you know what it takes to maintain a good credit score?

Test Your Knowledge Learn About Mortgage Loans

Do you open a lot of credit cards?

A

Yes

B

No

FICO Score

690